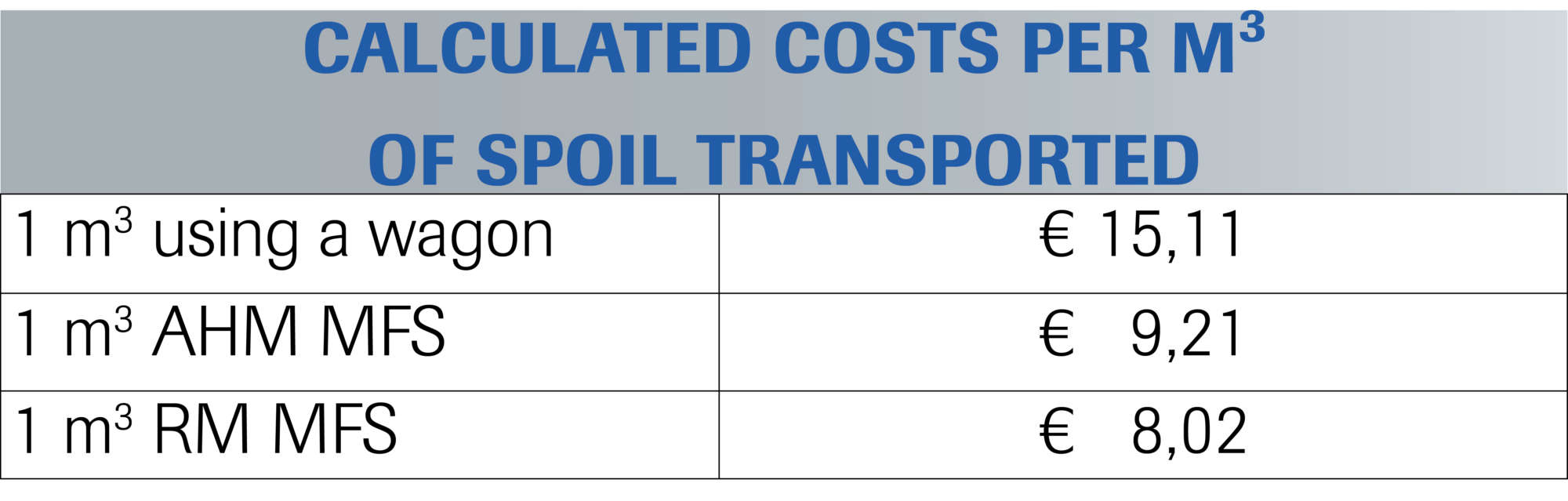

A specific comparison serves as an example: based on an excerpt from the annual performance of Austrian Federal Railways for formation rehabilitation and ballast bed cleaning in the year 2009 the following calculation was made. In the formation rehabilitation sector the AHM 800 R achieved an annual output of 102 km, for ballast bed cleaning the RM 80 UHR achieved 111 km.

A comparison shows the variation of spoil loading using standard flat wagons in contrast to loading using MFS units.

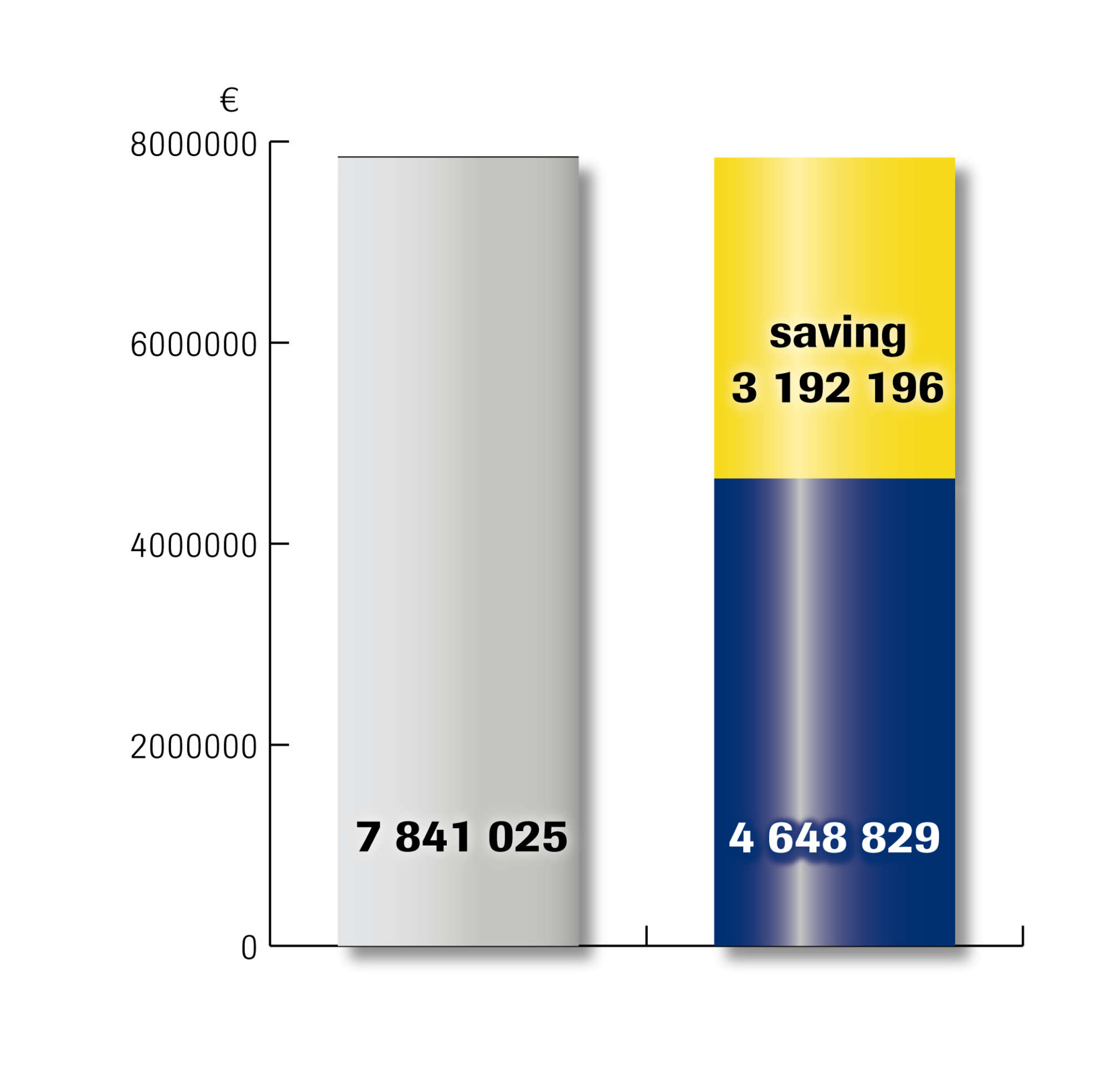

In general, it would be possible to unload the spoil quantities of both machines at the side, storing it for a limited period and then load it onto flat wagons with a storage capacity of 10 m³ and take it away.

With a total quantity of 519.000 m³ this would amount to 51,900 wagon loads. Taking into consideration the costs for providing the wagons, the work locomotives, an on/off-track digger for loading and the necessary workmen as well as the driver of the work train from the railways, in this example there will be costs amounting to € 7.841.025 (net).

(Not taken into consideration are the operational hindrance costs due to an extension of the construction project compared to the use of MFS units and the costs for worksite security and the line occupation.)

In Austria it is common practice to use MFS units for transporting waste material.

For the above calculation example this means the application of six MFS 100 for formation rehabilitation using the AHM 800 R and the application of three MFS 100 for ballast bed cleaning using the RM 80 UHR.

Taking into consideration the costs for hiring MFS units in the above quantity including staff, work locomotive and unloading station as well as work train driver of the railway, this example will incur costs amounting to € 4,648,829 (net).